by Bimal Mirwani and Michelle Leung

Exploring whether the rest of the world is sticking with fiat currency or shifting to digital payments.

Around the world, the way people pay for everyday goods and services is evolving with technological advancements. While traditional fiat currency – government-issued legal tender – has long been the backbone of commerce, digital payments are increasingly becoming the norm.

Asia-Pacific is leading this transformation, with 645.8 billion non-cash transactions recorded in 2023, surpassing Europe’s total (361.1 billion) and North America’s (237.3 billion). Latin America also shows substantial growth potential, particularly in Brazil, Peru and Colombia, driven by instant payment systems. Looking forward, digital payments are expected to generate USD 3 trillion in revenue globally by 2028, with Asia-Pacific accounting for nearly half of all transactions.

Hong Kong

Hong Kong is quickly moving toward a digital payment future. In 2024, over 85% of residents used e-wallets like Octopus, Alipay, WeChat Pay, and PayMe, making these platforms a regular part of everyday life. Octopus stands out with a 98% penetration rate across the city, covering everything from retail shops and restaurants to public transport. Hong Kong’s Faster Payment System (FPS) is also highly popular as it can be used 24/7 and enables instant, free transfers and payments through phone numbers, emails, or FPS IDs across banks and e-wallets. Looking ahead, digital wallets are expected to make up about 40% of all digital payments by 2025. Although cash is still used, an undeniable trend is taking shape – one that clearly favours digital payments.

Digital payment ratio*: 52% (e-commerce); 38% (point of sale)

Digital payment methods: Octopus, Alipay, WeChat Pay, PayMe, PayPal, Google Pay, FPS

Mainland China

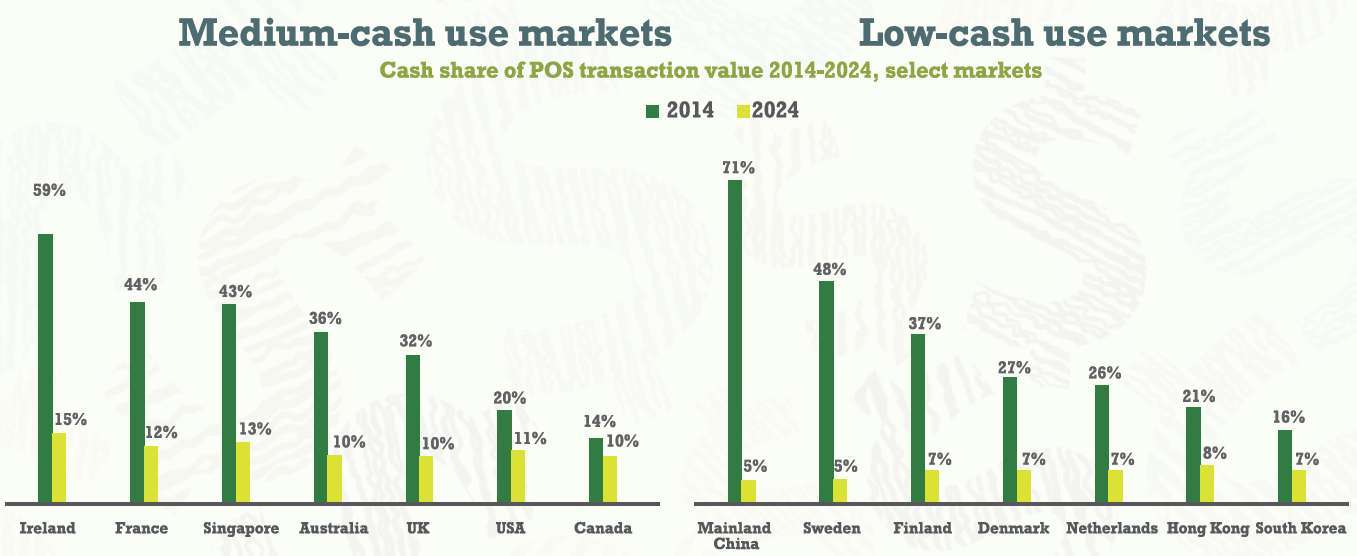

China has quickly become a mostly cashless society, with digital payments now the everyday norm. Mobile platforms dominate, handling over 90% of mobile transactions nationwide. People use QR codes to pay for everything – from street food to train tickets – with digital wallets deeply woven into daily life. While cash is still used in some rural areas and by small vendors, its role is shrinking fast. The government and fintech companies are pushing innovation with AI, biometric security, and 5G contactless payments to make digital transactions even more convenient and secure.

Digital payment ratio*: 90% (e-commerce); 74% (point of sale)

Digital payment methods: Alipay, WeChat Pay, QR code-based payments

Japan

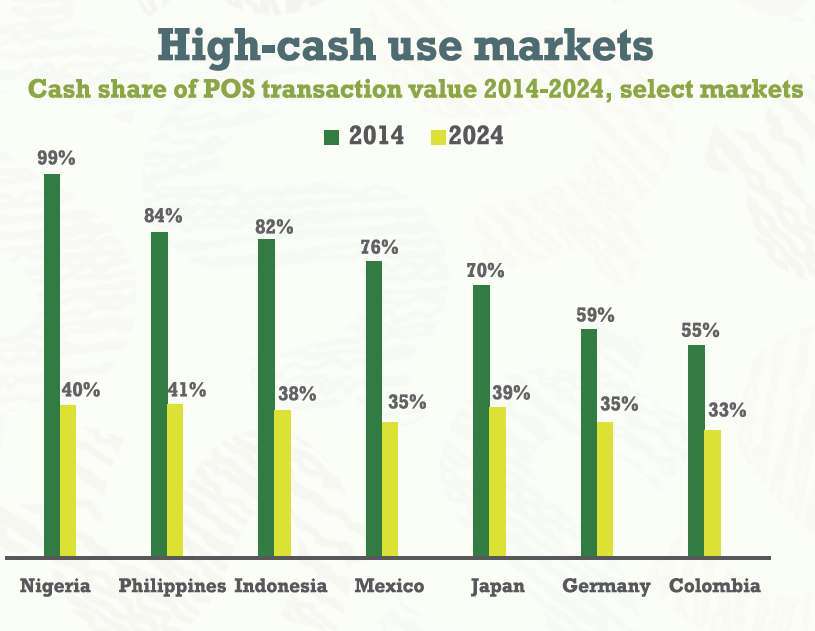

Japan has been a cash-focused society, which is believed to be associated with its ageing population. While the older generation prefers traditional ways, the younger generation widely uses cashless methods. Recently, cashless payments have been gaining ground. In 2024, 42.8% of all transactions were digital. Despite this, cash still plays an important role. One typical example of Japan’s traditional payment method is Konbini, which means “convenience store” in Japanese. It is a typical local cash-based payment method that allows customers to order products online and pay for them at a convenience store. To encourage digital payments, the government is offering incentives, improving infrastructure, and updating regulations. In the future, the Japanese government, while not specifying the time frame, says it aims to bring the cashless ratio up to 80%.

Digital payment ratio*: 33% (e-commerce); 25% (point of sale)

Digital payment methods: PayPay, Rakuten Pay, LINE Pay, QR code-based payments, Suica

South Korea

South Korea has firmly established digital payments as the norm. The country’s digital payments market is projected to reach nearly $198 billion in transaction value by 2025, with strong growth driven by mobile wallets, smartphone adoption, and a tech-savvy population that embraces contactless and QR code payments. The COVID-19 pandemic accelerated this trend. In addition, starting from April 2025, South Korea launched its central bank digital currency, the digital won “Hangang”, allowing participants to convert traditional bank deposits into the digital currency and spend at partner merchants. Despite the dominance of digital payments, cash has not been entirely phased out.

Digital payment ratio*: 41% (e-commerce); 25% (point of sale)

Digital payment methods: KakaoPay, Toss, Naver Pay, PayCo

Australia

Australia has seen a big shift from cash to digital payments, with digital methods now the go-to choice for many. In 2024, digital payments made up 53% of all e-commerce transactions, overtaking card payments and cash for the first time. This growth is driven by mobile wallets and the now-popular buy now, pay later services. Fiat currency accounted for just 13% of consumer transactions in 2022, down from 70% in 2007, and it’s expected to fall further to around 7% by 2030.

Digital payment ratio*: 58% (e-commerce); 24% (point of sale)

Digital payment methods: BNPL, Bpay, Apple Pay, PayPal, Google Pay

Papua New Guinea

Papua New Guinea has one of the highest unbanked populations globally, with about two-thirds of its population lacking reasonable access to formal financial services. This limits widespread adoption of digital payments. Despite this, steady progress is being made in the adoption of digital payments, thanks to mobile payment platforms like BSP. Papua New Guinea is also exploring a Central Bank Digital Currency, which is currently in a pilot phase. Supported by international partners, including Japan’s Soramitsu and Mitsubishi, this initiative aims to reduce reliance on physical cash, lower transaction costs, enhance security, and promote financial inclusion across both urban and remote areas.

Digital payment ratio: N/A

Digital payment methods: BSP, MiBank

United States

The United States is steadily shifting towards digital payments, though cash still plays a big role in everyday transactions. As of early 2025, about 53% of US consumers reported using digital wallets more often than cash or physical cards, and nearly 70% of online adults have used digital or mobile payments in the three months prior to March 2025. Mobile payments are expected to make up nearly 79% of all digital transactions this year, driven by convenience, speed, and security features like biometric authentication. Despite growing consumer use, many small businesses are slower to adopt digital wallets with less than 60% accepting them, compared to almost 95% supporting card payments. Cash usage, while declining, remains resilient due to long-standing consumer habits.

Digital payment ratio*: 50% (e-commerce); 19% (point of sale)

Digital payment methods: Venmo, Cash App, Apple Pay, Google Pay

UK

The UK’s payment landscape is evolving fast, with digital payments growing quickly, but cash is still holding its ground. In 2024, digital wallets, contactless cards, and instant bank transfers became more popular than ever, driven by consumers looking for convenience and security. The government’s National Payments Vision, launched in late 2024, aims to modernise the system with projects like the New Payments Architecture.

Surprisingly, cash usage has increased in recent years. Data from Nationwide shows cash withdrawals rose for the third year in a row in 2024. “The rising cost of living continues to impact people, and many are opting to budget with physical money to avoid getting into debt,” said Otto Benz, Director of Payments at Nationwide Building Society. Similar to most new technological innovations, market reports show that younger people are more likely to use digital payments and budgeting tools.

Digital payment ratio*: 52% (e-commerce); 19% (point of sale)

Digital payment methods: Apple Pay, PayPal, Google Pay, Samsung Pay

The Netherlands

The Netherlands has largely moved past cash, with digital payments now making up over 80% of all transactions as of early 2025. Mobile payments and contactless cards are especially popular for their speed and ease, while cash use at stores has dropped by about 20% since 2018. Digital wallets and online payment methods like iDEAL are growing fast, supported by high smartphone use and seamless integration with Dutch banks. While cash use has diminished, about 1.3 to 1.5 million people still depend on it for daily transactions as of 2020.

Digital payment ratio*: 88% (e-commerce); 33% (point of sale)

Digital payment methods: iDEAL, Klarna, SEPA Direct Debit

Argentina

Argentina is in the midst of a big shift from cash to digital payments. Digital wallets have grown rapidly from just 4% market share in 2017 to around 25% in 2024, and the share of respondents using cash transactions declined to 69% in 2024. This rise is largely thanks to platforms like Mercado Pago, which offer contactless and offline payment options. Interestingly, Argentina leads Latin America in mobile payment app usage, with 95% of the population using payment apps on mobile devices.

Digital payment ratio*: 50% (e-commerce); 34% (point of sale)

Digital payment methods: Mercado Pago, PayPal, Rapipago, PagoFacil

Ethiopia

Ethiopia is still largely a cash-based economy, but it’s making big moves toward digital payments as part of its Digital Ethiopia 2025 plan. The government, along with the National Bank of Ethiopia, launched its first National Digital Payments Strategy in 2021 to boost financial inclusion, make payments more efficient, and support economic growth. Despite these advances, cash continues to play an integral role in everyday life.

Digital payment ratio: N/A

Digital payment methods: Telebirr, CBE Birr, HelloCash, Amole

Antarctica

Antarctica doesn’t have an official currency or a traditional economy since it’s mainly home to temporary scientific and support staff from various countries. Transactions usually happen using the currencies of the countries running the research stations, with the US dollar being the most common because of the large American McMurdo Station. Any digital payments are mostly made through digital wallets such as Apple Pay and Google Pay, especially on expedition ships and at station facilities.

Digital payment ratio: N/A

Digital payment methods: Apple Pay, Google Pay

While the global momentum favours digital payments, the coexistence of fiat currency persists in numerous parts of the world, indicating that physical currency isn’t down and out just yet.

* Data from The Global Payments Report 2025: The past, present and future of consumer payments by Worldpay.

Financial Education Around the World

Many countries have now made financial literacy in education a priority. In 2015, Denmark made financial education mandatory for students aged 13 to 15, covering banking, budgeting, savings and more. This has resulted in Denmark’s impressive 71% financial literacy rate, one of the world’s highest.

In 2021, Japan revised its “Course of Study” to include financial education in secondary school home economics and civics classes, covering topics such as financial products, their features, and how to operate them, aiming to teach students financial concepts from a young age. Singapore’s primary and secondary schools also have dedicated financial education courses integrated into the formal curriculum, teaching key financial concepts such as distinguishing between “needs” and “wants,” budgeting, thrift, and saving to younger students; and through food and consumer education, helping secondary students learn how to be responsible and savvy consumers, including basic financial planning.iv

In the United States, as of the middle of last year, 16 states require what is called a “standalone personal finance course” for high school graduation, with “over a quarter of states (having) enacted financial literacy requirements.” Other countries with implemented financial literacy programmes in schools include, but are not limited to, Australia, in which this is included as part of the mathematics and personal development subjects, while in South Africa, it is part of the life skills curriculum. In Canada, the focus is on budgeting, savings and investing and in the UK, where financial education is part of the national curriculum.

■

Many countries have now made financial literacy in education a priority. In 2015, Denmark made financial education mandatory for students aged 13 to 15, covering banking, budgeting, savings and more. This has resulted in Denmark’s impressive 71% financial literacy rate, one of the world’s highest.

In 2021, Japan revised its “Course of Study” to include financial education in secondary school home economics and civics classes, covering topics such as financial products, their features, and how to operate them, aiming to teach students financial concepts from a young age. Singapore’s primary and secondary schools also have dedicated financial education courses integrated into the formal curriculum, teaching key financial concepts such as distinguishing between “needs” and “wants,” budgeting, thrift, and saving to younger students; and through food and consumer education, helping secondary students learn how to be responsible and savvy consumers, including basic financial planning.iv

In the United States, as of the middle of last year, 16 states require what is called a “standalone personal finance course” for high school graduation, with “over a quarter of states (having) enacted financial literacy requirements.” Other countries with implemented financial literacy programmes in schools include, but are not limited to, Australia, in which this is included as part of the mathematics and personal development subjects, while in South Africa, it is part of the life skills curriculum. In Canada, the focus is on budgeting, savings and investing and in the UK, where financial education is part of the national curriculum.